|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

|

|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

And lessons drawn from the first defeat

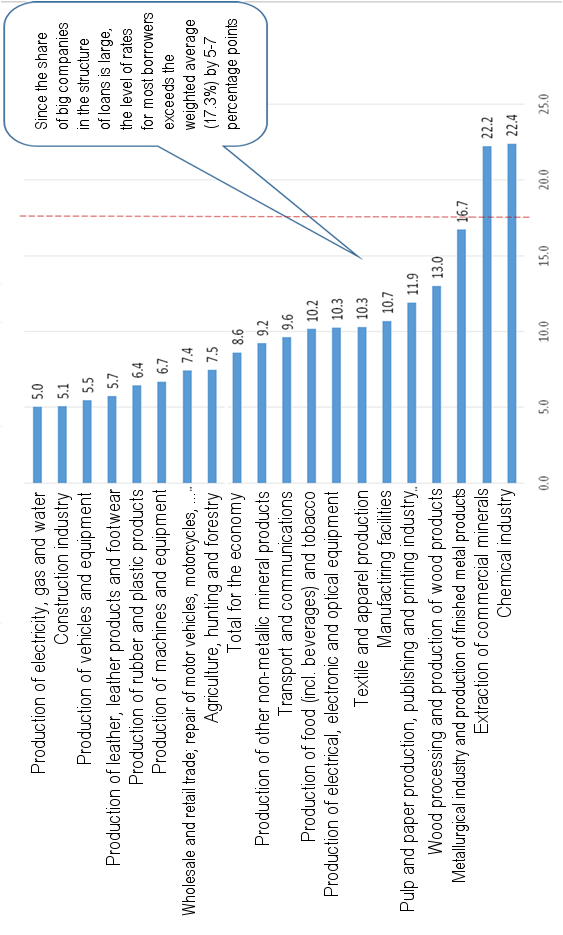

The conflictology of U.S. aggression against Russia was most visibly and tangibly manifested in the current financial and economic destabilization of Russia. It was explained above that modern war has a hybrid nature that combines financial, economic, information-psychological, diplomatic and military factors of damaging action. From legal point of view, the moment of its beginning on the part of the U.S. against Russia can be considered the adoption by Washington on March 17, 2014 of the resolution to impose economic (and personal) sanctions, grossly violating the international trade and economic laws established by the WTO. The key place in the ongoing hybrid war of the U.S. against Russia belongs to the financial and economic battlefront, on which the adversary (the U.S. and its allies) has massive superiority. They use their dominance in the world monetary and financial system to manipulate the financial market of Russia and destabilize its macroeconomic situation, to undermine the economy reproduction and development mechanisms. This is done by combining financial embargoes with speculative attacks against the Russian monetary and financial system. On the one hand, the U.S. authorities are blocking medium and long-term loans and investments of Western capital for the Russian economy. On the other hand, they do not limit short-term loans and investments, creating opportunities for speculative operations of any scale in the Russian market. As a result of the simultaneous outflow of long-term capital and inflow of short-term speculative liquidity, the monetary and financial system loses its stability and topples over into a turbulent mode. Due to the super-profitability of speculative transactions to manipulate the foreign exchange market, which involve large domestic credit and financial organizations and monetary authorities, a speculative funnel emerges that sucks the liquidity available in the economy. A significant part of the money issued by the Bank of Russia to refinance commercial banks was applied by the latter for financial currency speculations. Thus, the speculative funnel sucks out the foreign exchange reserves of the state. In an effort to preserve them, the Central Bank withdraws itself from the foreign exchange market, leaving it entirely in the hands of speculators. The most arrogant of them use their connections with the exchange to manipulate the market, boosting the drop of the ruble exchange rate to gain three-digit percent of profit on pre-planned speculative operations. The uncontrolled " bumps" of the ruble exchange rate throw the reproductive contours of the Russian economy locked to the external market into confusion, entailing inflation spikes and a drop in production. The loss of value reference points and a feverish state of the financial market make it impossible to expand the reproduction of the real sector of economy. Enterprises curtail manufacturing investments and channel the released funds to the financial market. Attempts by the Bank of Russia to stop speculation against the ruble by raising the key rate and contracting the money supply in a situation of turbulence in the financial market ultimately lock the monetary flows in a speculative funnel. The increase in interest rates on loans to a level many times higher than the profitability of the production sphere cuts off for the latter the access to bank loans (Fig. 10). The speculative vortex stops only after absorbing the entire amount of free money available in the market, after the amount of the money supply goes down much lower than the available currency reserves of the Bank of Russia. As always, simultaneously with the decline in the money supply, production and investment are falling, and the share of unprofitable enterprises and troubled loans is growing. This led to a sharp deterioration in the banking sector condition, where the aggregate capital deficit is estimated at 1.5 trillion rubles. The growing avalanche of bankruptcies of commercial banks is swallowing up the savings of many legal entities and individuals. Whereas the latter are awarded reparations, the amount of which approaches a trillion rubles, for tens of thousands of entrepreneurs these bankruptcies have fatal consequences. The Entrepreneurial Spirit Index has sunk to the lowest level for the last five years in a row. Instability and uncertainty have become the main factors of concern for the business community. Such actions of monetary authorities resulted in a significant decapitalization of the national economy, more than halving the turnover of the financial market, drastically cutting business activity and the volume of investments (up to 5% in GDP and up to 8% in investments in fixed capital). Thus, the goal of U.S. sanctions has been achieved, namely, to plunge the Russian economy into a crisis.

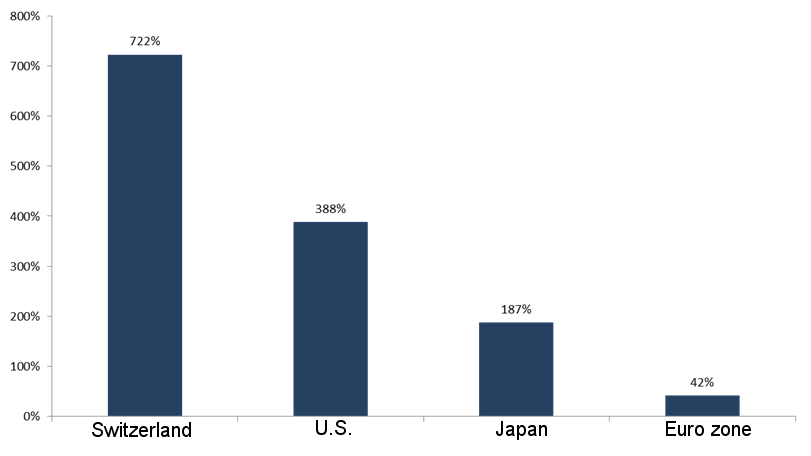

In the context of the ongoing quantitative easing policy pursued by the European Central Bank, which plans to continue issuing money at a rate of 60 billion euros a month, the monetary overhang of almost free loans is growing much faster than the possibilities for their absorption by the European economy. There is no doubt that part of this credit avalanche, despite the sanctions, feeds speculation on the Russian market as well. Although the Russian market is marginal for Western speculative capital (as its capitalization is 0.6% of the global figure), speculators do not shun the possibility of obtaining super-profits from its destabilization. The profit margin on speculative attacks in 1997-1998, 2007-2008, and in 2014 amounted to hundreds of percents, with Russia's GDP falling by 5%, or $70-80 billion year-on-year. Thus, the December attack on the ruble brought its organizers a speculative profit of $15-20 billion. Although the latter case involved credit support from the Bank of Russia, the role of non-residents in the Russian financial market remains the pivotal one. Their share prevails on the currency and financial market, accounting for 75-80%.

*Britain: 42%, calculated for the M0 aggregate. (Source: М. Ershov according to the central banks of the respective countries)

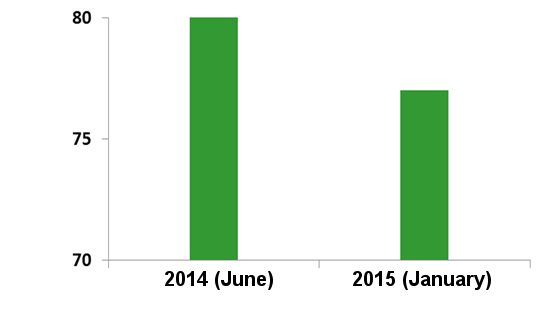

(Source: E. Obukhova. Svoego ne upustyat [They are in like Flynn]. Expert, 2015, No. 15. In Russian)

The dominance of non-residents in the foreign exchange market is complemented by control over the exchange itself. After the reorganization and privatization in favor of the largest foreign and Russian banks two years ago, Moscow Exchange (MOEX) slipped out of control of the Bank of Russia and turned out to be dependent on speculators. Many of its senior executives are affiliated with a number of large foreign and Russian financial institutions. It is no surprise that instead of acting as the central link in the infrastructure of the monetary and financial market responsible for its stable functioning in the general interest on a non-commercial basis, MOEX has become a center for profit generation on destabilizing the market under the pretext of " increasing its capitalization." In fact, MOEX has become the largest profit center in the Russian economy, with the volume of its last year's transactions exceeding $ 4 trillion, which is twice the size of the Russian GDP and an order of magnitude higher than all available deposits and cash in the country. Against the background of contraction of business, production and investment activities, the volume of transactions on the exchange doubled within the year, and their yield exceeded 70% per annum. At the same time, 95% of the MOEX turnover consists of purely speculative operations that are not relevant to the real economy. Due to the central position of MOEX in shaping the ruble exchange rate, and to the role of the latter in the formation of prices in the Russian market, the entire Russian economy appears critically dependent on non-residents. Their concerted actions can easily destabilize the macroeconomic situation, provoke the flight of capital, cause a decline in economic activity and investment. This is what allowed Obama to boast that the economic sanctions imposed according to his decision " left Russian economy in tatters." The available exchange information makes it possible to characterize the attack conducted against the Russian monetary and financial system as a pre-planned action in order to destabilize the macroeconomic situation. The targets chosen for the attack were the exchange rate determining the level of consumer prices and the interest rate affecting the financial position of enterprises. The attack of Western speculators on the Russian monetary and financial market was organized immediately after the introduction of U.S.-European sanctions and the shutting of external credit sources for Russian borrowers that owed $700 billion to non-residents. It began with manipulation to understate the pricing of their stock through the sale of depositary receipts on the London Stock Exchange in order to create conditions for the early termination of loan agreements. In parallel, Western creditors began withdrawing funds from Russia, creating a powerful pressure for depreciation of the national currency and contraction of money supply. This resulted in a reduction in the ability to refinance external debts of companies from the ruble sources of Russian banks. In this situation, the Central Bank's decision to switch to a free floating ruble exchange rate was perceived by all speculators as a signal to attack. They frenetically started buying up currency with a view to a collapse of the ruble rate, using the absence of the Central Bank in the market and their control over the exchange mechanisms. Contrary to the generally accepted world practice of market stabilization, during the whole speculative attack MOEX did not take any stabilizing measures, increasing the guarantee provision for futures contracts from 5.5% to 12% only at 7 PM on December 16, after termination of the main trading, when " the game had been already done." There was a fair reason to believe that a number of pre-positioned MOEX officials played into the hands of speculators, implementing that day several techniques that allowed to " transpose" of the ruble-dollar rate from 60 to almost 80, ensuring forcible closing of positions and super-profits for masterminds of the attack on the ruble. One way or another, the fact remains that MOEX did not employ any of the tools generally accepted in the world to stop the speculative attack on the ruble in December 2014. Moreover, the procedures for speculative operations crediting effective at the exchange made it possible to increase their power several-fold (option and futures trading allows a leverage to the capital of brokers of 1 to 10-15). The refinancing mechanisms of the Bank of Russia operated in a similar fashion, and through them, most of the issued loans were used to finance currency speculation (primarily by building REPO pyramids on the debt market). At the same time, the Bank of Russia participated in this attack both by its inaction (as the mega-regulator of the financial market in general, and as the controller of MOEX in particular), and by switching to a floating ruble exchange rate according to the predetermined algorithm. The organizers used the Central Bank as an " elementary automaton" for financial servicing of the speculative attack. A prerequisite for the success of this attack was the neutralization of the Central Bank as an independent player capable of influencing these parameters. To do this, the IMF imposed on the Bank of Russia recommendations to switch to " inflation targeting", removing from the monetary policy toolkit the means for currency regulation and control over cross-border capital flows, as well as over stabilization of the exchange rate. The latter was reduced to using one tool only, that is, the key rate. A substitution of the target parameters of monetary policy had been accomplished in advance, excluding from them the Central Bank's constitutional obligation to ensure the stability of the national currency and replacing it by the consumer price index. After these conditions had been created, sanctions were declared, and the withdrawal of capital began. It was followed by the attack on the ruble in order to slump its exchange rate and create panic to provoke the Central Bank to raise the key rate, which automatically resulted in an avalanche of economic problems, such as credit squeezing, investment and production losses, failures of banks and businesses, an unemployment and inflation spike, which immediately led to a decrease in household income and a worsening of the socio-political situation. The destabilization of the macroeconomic situation stopped investment activities. Impairment of ruble assets and appreciation of foreign currency liabilities made a significant part of commercial banks cross the red line of capital adequacy, putting the financial and banking system on the brink of collapse, to avoid which the state had to allocate 2 trillion rubles at the expense of budget cuts and a corresponding reduction in final demand. As follows from the foregoing, the Russian monetary authorities turned out to be unable to control the situation on the monetary and financial market. Large-scale manipulations of this market are planned from outside by Western megaspeculators who control Moscow and London stock exchanges, as well as the depository and clearing centers EUROCLEAR and CEDEL. The macroeconomic achievements of the last 10 years have been undermined by the professional action that was planned, calculated and implemented by the decision of the U.S. leadership, striking the Central Bank (the management of which blindly complied with IMF recommendations) with cognitive weapons. Two-fold depreciation of the national currency and an increase in the credit rate plunged Russian economy into a stagflation trap and into a turbulent mode of the financial market operation. This entailed a profound disorder of the whole system of reproduction and knocked the Russian economy from the trajectory of rapid and sustained growth down into a man-made crisis. This attack could have been prevented, had the Central Bank after the announcement of U.S.-European sanctions introduced measures of bank and currency control to protect our financial system against external attacks. Instead, it actually acted as their tool, announcing in advance the refusal to maintain the ruble exchange rate at the target level. The negative effect of stabilizing the ruble exchange rate with its sharp 1.5-fold decline unexpected for speculators would have been an order of magnitude smaller than today's problems. The Central Bank would have spent $50 billion from reserves to maintain an objectively conditioned exchange rate, the speculative attack would have been drowned, credit expansion at an unchanged rate would have quickly ensured import-substituting production growth and price stabilization, as it was in 1999. Disconcertingly, in the absence of an effective system of state regulation, the monetary and financial market not only fails to fulfill the function of forming productive investments, but also is a source of destabilization of the Russian economy. In respect of the major part of transactions performed therein, the use of insider information can be traced. Typical examples include market manipulation not only by large-scale currency attacks planned with a full understanding of the Central Bank algorithm, but also through mass effectuation of sham deals with securities resale cycles at inflated prices. The stock market rocked in such a way loses its connection with the real sector, the prices formed on it do not reflect the real value of assets, and it ceases to be a reference point for bona fide investors. In fact, it is manipulated by mala fide players, an active role among which is played by foreign foundations that have unrestricted access to loans from the U.S. Federal Reserve and the ECB. Controlled by speculators, the Russian monetary and financial market acts as a funnel, dragging out the money available in the Russian economy to enrich speculators at the expense of savings and income of Russian citizens and manufacturing enterprises. The monetary authorities proved unable to resist the financial market manipulations due to both their refusal to use the generally accepted regulatory measures and the monetary policy pursued. The " inflation targeting" policy was reduced to a refusal to use currency restrictions and to limitation of the whole variety of available monetary policy instruments to one only, that is, the key rate. However, in conditions of full openness of the monetary and financial market, the increase in interest rates does not operate to reduce inflation and stabilize the ruble exchange rate, as foreign speculators and insiders manipulating the financial market obtain a much higher profit margin. The predictable result of the " stabilization" policy of the Bank of Russia is squeezing of credit for the real sector of the economy, and a fall in production and investment, which in turn leads to an increase in costs and, accordingly, inflation. The current condition of the Russian monetary and financial system can be described as unmanageable. The administrative decisions of monetary authorities lead to results that are opposite to the planned ones. The main political consequence of the pursued monetary policy is the manipulation of the Russian monetary and financial market by foreign financial institutions associated with issuers of world currencies. The chaos created by them suppresses administrative stimuli on the part of monetary authorities. Contrary to the declared intentions, the main economic consequence of their policy is enrichment of market participants that speculate on destabilizing, due to depreciation of savings and income of citizens and industrial enterprises, and to outflow of capital from the real sector and abroad. The continuation of this policy is incompatible with the independent political course and national security of Russia, which is being attacked by the U.S. and its allies. It follows from the foregoing that in order to ensure the security and sustainable development of the Russian economy, it is necessary to protect it against destabilization with external factors, primarily against attacks from foreign speculators associated with the U.S. Federal Reserve and issuers of other world currencies. This implies adoption of selective restrictions on the cross-border movement of speculative capital. Such restrictions could include measures of both direct (licensing, reservation) and indirect (capital transfer tax) regulation. A response to Western sanctions may take the form of a moratorium on cross-border short-term transactions, including a ban on servicing loans and investments from countries practicing anti-Russian sanctions and seizure of Russian assets. Along with the introduction of selective restrictions on cross-border speculative transactions, it is advisable to take measures long proposed by the RAS scientists for economy deoffshorization and dedollarization, along with stabilization of the ruble exchange rate. Serious efforts are also necessary to regulate the financial market and protect it from the potential use of insider information and other manipulative actions. It is important to block the possibility of involving employees of state banks and companies in sham deals. Only after introduction of protective measures specified above, as well as after restoration of control over the key nodes of the national financial infrastructure, including MOEX, can the work of the monetary and financial market be normalized, and a monetary and credit policy oriented to the growth of production and investment be implemented.

Section 4 HOW COULD THE WAR BE PREVENTED? To prevent the war, it is necessary to convince the aggressor of the unattainability of its goals. To this end, first of all, it is necessary to establish an international coalition, against which the aggressor objectively will not be able to win the war. Secondly, the coalition members ought to have a common understanding of threats and a vision of the future, which requires development of a common understanding of the laws of socio-economic development. Thirdly, they need the common goals and development programs that would unite them. And, of course, measures should be taken to weaken the aggressor. It must be deprived of the opportunity to violate international law unpunished.

|

Последнее изменение этой страницы: 2019-06-09; Просмотров: 146; Нарушение авторского права страницы

Fig. 11. Increase in the monetary base of the currencies of countries in 2007-2014 (calculated by national currencies), %.

Fig. 11. Increase in the monetary base of the currencies of countries in 2007-2014 (calculated by national currencies), %. Fig. 12. The share of non-residents in the Russian stock market, %.

Fig. 12. The share of non-residents in the Russian stock market, %.