|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

|

|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

The financial war against Russia

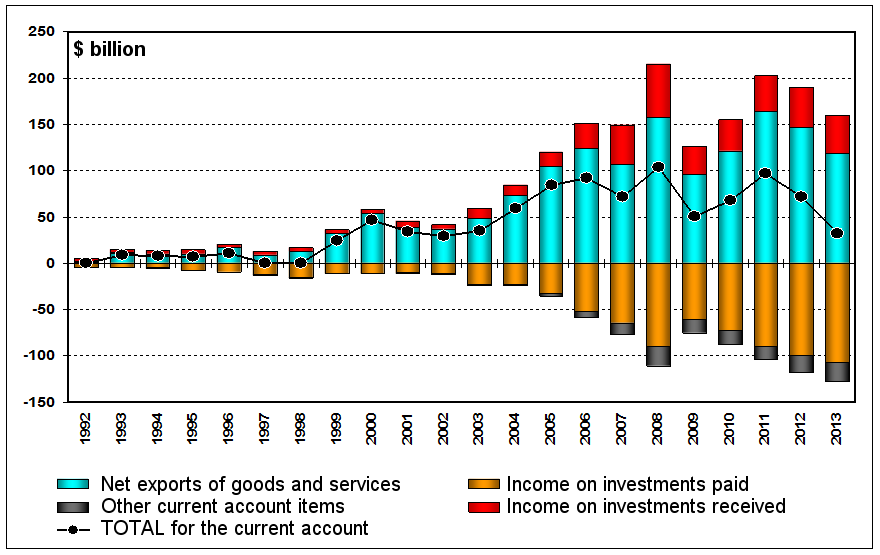

Western sanctions include an almost complete set of tools for economic, political and informational pressure on Russia, beginning with its ruling stratum (broadly interpreted, including not only political but also regional and business elites), and ending with solid citizens who are facing an impairment of their savings. The Russian assets under the jurisdiction of the U.S. and its allies are subject to various encumbrances. The capital flight from Russia is encouraged, and by the end of 2014 its scope almost tripled relative to the already abnormally high level. International payments are hindered, Russia's sovereign credit rating is declining, many economic projects with Western corporations are being suspended, foreign trade is being curtailed, and access to advanced technologies is being blocked. Simultaneously with introduction of the next package of sanctions against Russia on the part of the U.S. and the EU, the Bank of Russia adopted on July 25, 2014 a resolution on another increase in the base lending rate to 8% per annum. Both these decisions had similar consequences, that is, worsening of the already unsatisfactory lending conditions for Russian business. Whereas the motivation of U.S. lawmakers is clear and consists in inflicting damage to the Russian economy that chokes on the chronic shortage of long-term loans, the motives of the Bank of Russia raise questions. The Bank of Russia motivated its decision to raise the interest rate by the fact that " inflation risks have increased due to a combination of factors, including, inter alia, the aggravation of geopolitical tension and its potential impact on the ruble exchange rate dynamics, as well as potential changes in tax and tariff policy" [217] (On the Bank of Russia Key Rate, July 25, 2014). In so doing, the Bank of Russia has tried to justify its attempts to neutralize the factors independent of it, exacerbating their negative effect on the already declining business and investment activity. The experience of such a macroeconomic policy in Russia and other countries with a transition economy shows demonstrates that it inevitably results in stagflation, that is, a simultaneous drop in production and an increase in inflation[218]. This is exactly what is happening now: after the previous increase in the refinancing rate in April, the country's economy plunged into depression against the backdrop of revival of economic activity in neighboring countries. The management of the Bank of Russia associated its previous decision to raise the key rate, with which it had replaced the refinancing rate, with " more pronounced than expected pass-through effect of the exchange rate dynamics on consumer prices, the rise in inflation expectations, as well as unfavorable conditions in the markets for some goods." [219] Although, like this time, it explained its decision by external factors, the first two of them were actually generated by the actions of the Bank of Russia itself, which refused to target the ruble exchange rate and limited the refinancing of commercial banks with three months, and also provoked the banking crisis by an unexpected recall of licenses from many regional banks. Later, the Central Bank raised the key rate a couple more times, bringing it to 17% and paralyzing the crediting of the real sector. As scientists and experts warned, this decision resulted in a sharp drop in business and investment activity, an increase in the costs of enterprises, and an upsurge of inflation. The inadequacy of the Bank of Russia's policy with respect to the tasks of economic growth has already become a habitual point of its criticism, which the management traditionally meets with monetarist dogmas. However, provided that until now the price of the incompetence and dogmatism of the monetary authorities was the fall in production and export of capital, accompanied by degradation of the economy structure, the suppression of external sources of credit challenges its very existence. Absence of credit makes not only expanded, but even simple reproduction of the modern economy impossible. The policy of linking monetary issue to the growth of foreign exchange reserves has led to the fact that the bulk of the monetary base became formed for foreign sources of credit, and the amount of the external debt of the Russian economy exceeds the scope of domestic credit. The transition to monetary emission through the channel of commercial banks refinancing without monitoring the targeted use of allocated loans has not changed the situation, since the short term and high cost of these loans makes them inaccessible for production enterprises, and they are mainly used to fund currency speculations. The monetary policy pursued by the Bank of Russia entails degradation and excessive external dependence of the economy. The Bank of Russia's persistent unwillingness to create domestic long-term credit forced the largest banks and corporations to borrow abroad, mainly in the EU and the U.S. The termination of refinancing from the latter due to sanctions threatens to destroy the mechanisms of reproduction that have been established in the Russian economy. To avoid this, the Bank of Russia should have promptly deployed mechanisms for long-term refinancing of Russian borrowers, capable of replacing the external sources cut off by sanctions. These mechanisms should be comparable to European and American ones that provide unlimited refinancing of Western banks and corporations on a long-term basis at a symbolic interest rate. Instead, the Bank of Russia raises the interest rate and narrows the variety of refinancing facilities, limiting them to short-term operations for liquidity support. In so doing, it sharply exacerbates the negative effect of Western sanctions, condemning the still unharmed sectors of the Russian economy to contract production and squeeze investments. Anti-Russian sanctions and a wave of tightening of the Bank of Russia's monetary policy are entering a resonance posing a serious threat for the Russian economy. Raising the interest rate, the management of the Bank of Russia proceeds from dogmatic ideas that the rise in the cost of the resources provided to the banking system reduces inflation. However, as shown by numerous studies, monetary factors of inflation are not the main ones under modern Russian conditions. Moreover, it has been proven both theoretically[220] and empirically[221] that attempts to suppress inflation by tightening the quantitative limits of monetary issue or increasing the price of credit do not provide the desired result in the modern economy with its complex feedbacks, nonlinear dependencies and imperfect competition. For two decades already, these attempts have been showing their futility: instead of lowering inflation, there is an invariable fall in production and supply of goods and, as a consequence, price increases. The Bank of Russia's policy is based on very primitive ideas about the linear relationship between monetary issue and inflation, ignoring complex feedbacks that mediate the transformation of money into a commodity in the process of expanded reproduction. The quantitative theory of money, taken by the management of the Bank of Russia as a premise, completely disregards the process of production, as well as scientific and technical progress, monopolies, external competition and other factors of the real economy[222]. This multiply disproved theory is a set of dogmatic statements that are reduced to the justification of quantitative restrictions on the issue of money as the only way to reduce inflation, which, in turn, is declared the sole purpose of monetary policy. It is not difficult to prove that if some country imposes strict restrictions on the issue of money at a level that is obviously inadequate for its expanded reproduction, ensuring at the same time free cross-border movement of capital, then the domestic capital is pushed out by the foreign one, which the world currency issuers can provide at any interest rate and in any amount. Such economy becomes externally dependent and evolves towards external demand for its products. A while back, the author has shown[223] that following the monetarist dogma entailed the degradation of the Russian economy, the decline of the investment complex targeted at domestic demand (machine building and construction), and the excessive growth in exports of primary goods due to a squeezing of their domestic consumption. The scientific press repeatedly demonstrated the absence of a statistically significant relationship between money supply growth and inflation; there are many examples of a negative correlation between these indicators at the stages of economic growth, including Russia in the 2000s (the bibliography may be taken, for example, from the Russian Economic Journal)[224]. However, the Bank of Russia consistently ignores both non-monetary factors of price changes and the reverse effect of credit appreciation on price increases and inflationary expectations. This ignoring of the obvious is indicative of either incompetence, or commitment of the management of the Bank of Russia to certain interests that are alien to it. No matter how the monetary authorities tried with science-like rhetoric to represent the policy pursued by them as objectively conditioned, in reality it is highly subjective and directed contrary to the interests of the development of the Russian economy. Economic policy is never neutral with respect to economic interests. It is always pursued in the interests of dominant influence groups, which do not always correlate with the national interests. For example, the Washington Consensus policy implemented in Russia for a quarter of a century already is being imposed by the IMF on developing countries and countries in transition in favor of international capital, contrary to their national interests[225]. We also observed its consequences in Russia in the 1990s, when the Bank of Russia's policy was simultaneously killing high-tech economy sectors and generating unprecedented profits for foreign (mostly U.S.) speculative capital[226]. A similar situation is emerging today. In a climate of escalation of external pressure and disconnection of Russian borrowers from global capital markets, the increase in the rate raises the cost of credit and aggravates the risks of defaults for borrowing companies. Instead of creating a mechanism for replacing external sources of credit with internal ones to cover the credit resources shortage arising because of sanctions, the Bank of Russia only exacerbates it. At the same time, while maintaining a free regime for cross-border capital operations, it contributes to the export of capital, which has already exceeded $ 200 billion since the introduction of sanctions. Taking into account the currency reserves spent on support of the ruble exchange rate, the Russian financial system has lost more than four trillion rubles as a result of this monetary policy. It is interesting that the amount of illegal capital flight, which amounted to more than $ 80 billion in the first half of the last year, coincides with the reduction in foreign loans to Russian entities due to sanctions. Thus, the negative effect of sanctions could have been completely neutralized by cessation of the illegal capital flight, for which the Central Bank has every opportunity. However, acknowledging the acceleration of capital flight, the Bank of Russia refuses to apply the currency control regulations necessary for its termination and carries on its passive abidance by the dogma of " full freedom of current and capital operations" [227]. The raising of interest rates in the current conditions of increased foreign economic risks cannot serve as a sufficient incentive to restrain capital outflows and stimulate its inflows. It only exacerbates the uncompetitiveness of the Russian banking system relative to the banks of the OECD countries that have cheap and long-term credit resources, provided to them by their central banks virtually free of charge. The preferential status of foreign creditors is enshrined in the regulatory policy of the Bank of Russia, which assesses the obligations of foreign jurisdictions (including offshores) with a lower discount than the obligations of Russian issuers on the grounds that the latter have a lower rating of the U.S. " Big Three" rating agencies. The monetary and credit policy pursued in Russia objectively entails colonization of the Russian economy by foreign capital. As A. Otyrba and A. Kobyakov justify in their analytical report How to Win Financial Wars, " the policy pursued by the Bank of Russia and the Government for a quarter of a century already is to create favorable conditions for foreign capital in reclaiming the Russian economy and the national wealth of Russia" [228]. Within the framework of this policy, advantage belongs to the foreign capital associated with the issuance centers of world currencies in connection with the fiduciary (fiat) nature of the latter. They are created without any actual backing, which is replaced by debt obligations of the respective states and corporations. Therefore, they can be issued without any restrictions and at any interest in the interests of these states and their national capital. The authors explain that the creation of modern fiduciary money is the most profitable type of economic activity due to obtainment of issuance revenues (seigniorage), which goes to the entity with which the money issuer makes the first transaction. In the U.S., these are the commercial banks linked to the Federal Reserve, in the EU, the issuing states of bonds accepted as security of ECB loans, in Japan and China, the governmental credit institutions, most notably development institutions. It is the issuance revenue generated when fiduciary money is created that turns up to be the energy of money, the main economic tool of the state which feeds energy to the national economy as well. Seigniorage advances the creation of added value, generating economic energy. The authors rightly point out that modern fiduciary money and capitals created on its basis are the most effective tool of economic expansion, allowing to claim the resources of other countries and exploit their peoples with minimal costs. The authors associate the fact that the victims of such policies, including Russia, do not hinder penetration of such money and capitals into their economic space, and even make efforts to attract them, with a low level of financial competence. Thus, Russian monetary authorities went unreflectively on a leash of the IMF and the experts of the U.S. Treasury, which indoctrinated them with dogmas advantageous for the latter. The essence of these dogmas consisted in conducting money issue in order to purchase foreign currency reserves (mostly dollar ones) and its limitation by the volume of their growth. In this case, the national currency becomes a surrogate of the dollar, and the national economy is subordinated to the interests of U.S. capital, the investments of which become the main source of domestic credit. The sectors in which foreign investors take no interest are shut out from loans and fall into disarray. The economy evolves under the decisive influence of external demand, acquiring raw material specialization. If the national bank issues money through acquisition of the currency of another country, then the issue revenues are received by the latter. The prime cost of money, in addition to the costs of its production and maintenance, includes also the cost of products paid by the currency bought by the central bank, which allegedly functions as backing of the former. In fact, it is earned money with a high prime cost, which makes both money itself and the capitals generated on its basis uncompetitive. Not only are they unable to ensure development, but they are also a tool for latent robbery of independent countries by the colonialists. The latter strictly control the two most important procedures of the country's monetary circulation, the injection of money into the market and its collection. And they can, by collecting money and stopping its injection, arrange a financial crisis and plunge the country into chaos. This is the situation that we have today. The U.S. authorities cut off the Russian economy from external sources of credit, and our own monetary authorities, instead of replacing them with internal sources, deal the final blow to the economy by making domestic credit more expensive. As surveys of enterprises show, most of them do not have the money to implement innovative projects[229]. Within the framework of the policy pursued by the Bank of Russia, the problems with money had not been experienced prior to the introduction of sanctions only by export-oriented raw materials corporations that could borrow from U.S. or European banks against pledge of their export earnings and assets. They can also borrow in the domestic market, as long as they have a sufficiently high profitability. At the same time, enterprises of the investment complex (machine building and construction) do not have access either to external sources of credit, or to domestic ones which are too expensive for them. At the same time, the funds insufficient for investment are streaming in a 150 billion annual flow from Russia abroad, usually without interest and taxation. Each year, Russia gives the world a hundred billion of cheap money to attract only half as much in expensive funds. The difference in interest rate alone makes it lose annually $ 40-45 billion in favor of U.S. and European creditors (see Fig. 13 on the transfers of Russia in favor of the global financial system on page 358). For many years, the Bank of Russia has been pursuing a restrictive monetary policy, artificially hooking the economy on the external sources of funding. Before the financial crisis of 2008, more than half of the money supply was formed from external sources, the main of which were the U.S. and EU issuance centers[230]. Not surprisingly, immediately after the outflow of foreign capital the financial market collapsed threefold, and the largest Russian corporations addicted to foreign loans would have been bankrupt, had it not been for unsecured loans granted to them by resolution of the government. The source of the latter was a trivial money issue aimed at replacing the withdrawn foreign loans. Despite its huge scope (about 2 trillion rubles), the country did not experience any significant inflation surges. Had the Central Bank in addition monitored its intended use, there would have been neither a fall in the ruble rate arranged by banks to derive super-profits from currency speculation, nor a decline in production that reached 40% in machine building. The question arises, what prevents the Russian monetary authorities from extending credit to the economy in the required amount, without losing a half of the financial market to foreign creditors? Why was it possible in 2008 to quickly replace foreign loans with domestic ones, and now, under sanctions, this cannot be done? And why did the monetary authorities immediately after the relative stabilization of the financial market rebound to restrictive monetary policy, withdrawing a significant part of the granted loans and recycling the economy back to external funding sources? The Russian external debt has increased by 2014 by more than $ 90 billion, reaching $ 730 billion. Servicing these loans, the financial system of the country is losing huge amounts of money. Thus, the negative investment income balance amounted to $ 66.7 billion last year[231]. Side effects of external dependence are offshorization of the economy and transfer of Russian property to foreign jurisdictions, since it is easier to take foreign loans against offshore security. Offshorization, in turn, results in outflow of capital, together with making a large part of the proceeds exempt from taxation. It is unlikely that such a policy of subsidizing the financial systems of the U.S. and the EU complies with the national interests of Russia, against which these countries declared a war. The experience of the 2008 crisis revealed a high degree of dependence of the Russian economy on the global financial market regulated by methods discriminatory for our country, including downward biasing of credit ratings, unequal demands for openness of the domestic market and compliance with financial constraints, and imposition of inequivalent foreign economic exchange mechanisms. In this situation, considerable advantages are gained by foreign capital, which can boundlessly dominate the Russian financial market. The economic science knows well that there is a reasonable limit to foreign investments, upon achievement of which their further build-up results in a retardation of economic growth due to excessively increasing payments for their servicing. Judging by the balance of income from investments received from abroad that has been paid to non-residents, this limit has long been passed. In some sectors, payments for servicing and payback of foreign investments already exceed their inflow. At the same time, about 70% of foreign investments are provided from offshores by the selfsame Russian business. It turns out that the relationship of the Russian financial system with the outside world substantially consists in circulation of fairly Russian capital, withdrawn to offshores without paying taxes and then partially returned to the country. In so doing, about half of the capital that leaves Russia ends up abroad following its owners who buy elite real estate and acquire foreign citizenship. The policy pursued by the Bank of Russia encourages offshorization and compradorization of Russian business. The entrepreneurs severed from external sources of funding find themselves in a obviously losing situation.

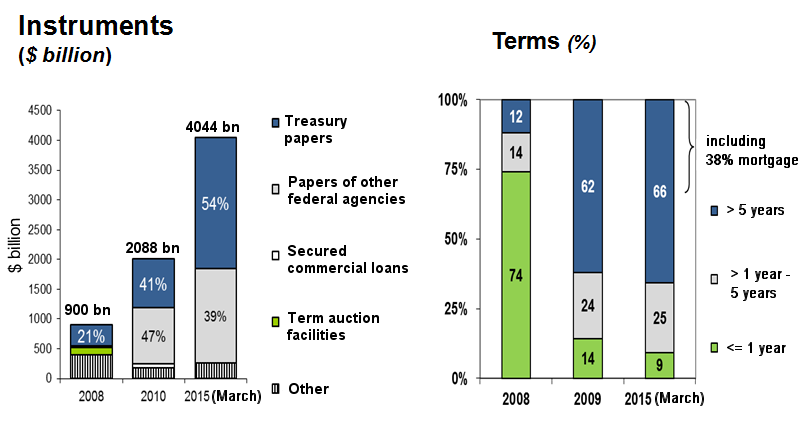

(Source: Y. Petrov) As has been shown, the nature of the world war being unleashed by the U.S. is, for the time being, mainly economic. The U.S advantage in this war rests upon the unlimited issuance of dollars, which ensures not only the unbelievably inflated military and foreign policy expenditure, but also the competitive strength of its economy consisting in unlimited free access to credit. In a situation where traditional methods of tariff protection are severely restricted by the WTO, it is the terms of crediting the economy that become the decisive tool of international competitive struggle. The advantage in doing this goes to countries that implement it using cheap money issued against their debt obligations. This entails a need for a drastic change in the money issue, switching it from being backed by foreign currency to the basis of internal obligations of the government and business. It should be noted that the Bank of Russia formally renounced in recent years the foreign currency backing of money issue. Its main part is directed through refinancing channels against security of the national borrowers. However, the problem is that this refinancing remains short-term and extremely limited. While the re-financing in countries with sovereign monetary systems is carried out at a symbolic, often negative interest rate and against long-term obligations of domestic borrowers, most notably the states themselves (the figure gives the structure of securing the dollar issuance as an example), the Bank of Russia limits its operations to weekly and monthly periods at a high interest inaccessible to most manufacturing enterprises (Fig. 16, 17). In other words, while financially sovereign countries apply money issue to credit production and investment activities, the Bank of Russia utilizes it only to support liquidity. The scale varies accordingly: whereas the European Central Bank has issued within a single round a trillion euros for three years to support economic activity, the increase in the Bank of Russia's liabilities is limited to several billion rubles a year, without any significant impact on the business activities.

(The basis of the entire issue are budget priorities: the monetary authorities (the Treasury – the Fed) are at the source of the formation of long money) *Others include float, swaps, gold, loans, etc.

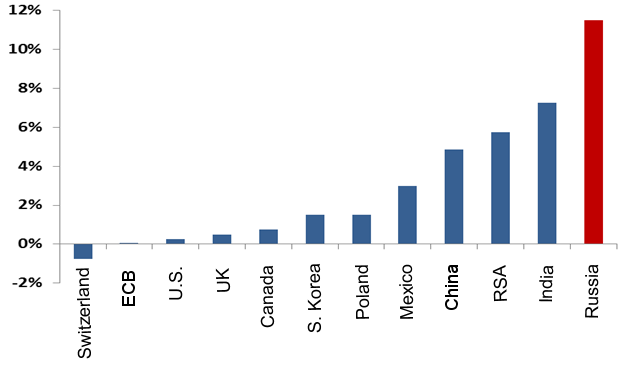

Fig. 17. The base rates of central banks, July 2015, %. (Source: М. Ershov according to data of the central banks) As shown by V.E. Manevich[232], the policy of monetary authorities is reduced to a kind of teeter-totter to support liquidity: during the first three quarters it is carried out from the budget accumulating income in bank accounts, and in the last quarter the Bank of Russia assumes this role by compensating the outflow of money from the banking system to discharge current budget obligations. Formally, the Central Bank does not resort to administrative restrictions on the growth of monetary aggregates, using the key rate of the Bank of Russia as the main tool to regulate the supply of money. However, the Bank of Russia acknowledges that it continues to be guided by quantitative restrictions in determining the amount of money issue, arbitrarily setting " the maximum amount of money provided at auctions" (to provide credit resources for a week on repo transactions, which constitute the main part of the flow of money issued by the Bank of Russia)[233]. This money is intended for the current balancing of demand and supply of liquidity in the banking sector, and is not supposed to be used as a source of credit for the production sector. The bulk of the flow of credit resources for these purposes continued until recently to come from abroad, burdening the Russian financial system with growing obligations. The total losses of the country's financial system due to the policy of the Bank of Russia are estimated by various experts as $ 1.5 trillion by the accumulated capital outflow, and taking into account the indirect losses due to underfunding of domestic investments, twice as much. We should add to this a twofold decline in industrial production due to the same policy of the Bank of Russia in the 1990s[234], as well as a 1.5-fold underinvestment in the development of the economy compared with the opportunities available in the aughties. The consequence of this policy was a threefold (record-setting by global standards) collapse of the financial market in 2008, and a sovereign default in 1998. These disasters could have been avoided with a reasonable monetary and credit policy serving not the interests of foreign capital, but the goals of the country's socio-economic development that had been repeatedly set at the highest level. The volume of GDP in Russia would have been one and a half times higher, the standard of living – two times higher, and the amount of accumulated investments in modernization of production – five times higher than today, had the Central Bank busied itself with development of domestic sources of credit to support the national economy. The sharp hydrocarbons price boost gave Russia an opportunity to preserve its sovereignty, which was used by President Vladimir Putin in order to restore the country's statehood in the administrative and political sphere. However, in terms of macroeconomic policy Russia is still a country dependent on the issuers of world currencies, which rigidly dictate their interests through the relevant monetary and credit policy.

|

Последнее изменение этой страницы: 2019-06-09; Просмотров: 166; Нарушение авторского права страницы

Fig. 15. The balance of income from investments received from abroad that has been paid to non-residents

Fig. 15. The balance of income from investments received from abroad that has been paid to non-residents Fig. 16. Monetary base of the U.S. dollar, $ billion, %.

Fig. 16. Monetary base of the U.S. dollar, $ billion, %. (Source: M. Ershov)

(Source: M. Ershov)