|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

|

|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

Springs of the mechanism of external influence on the Russian economy

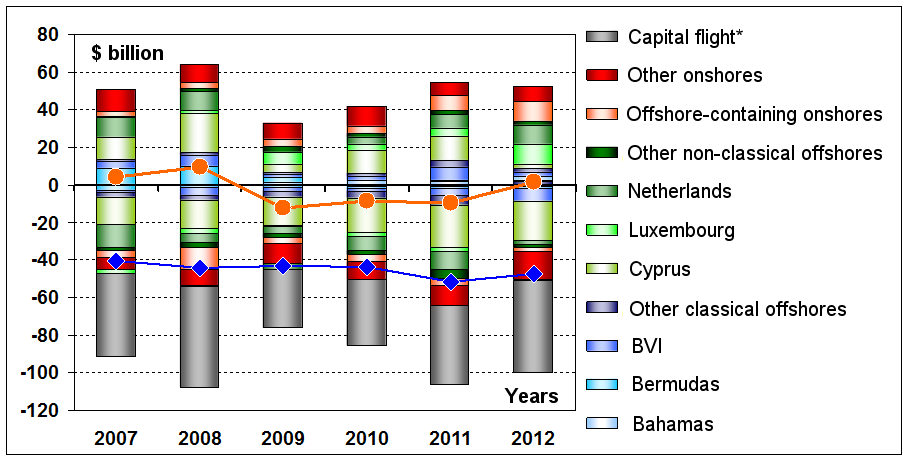

The status of the monetary system created in Russia in relation to the global one can be compared to a puddle connected by channels with large lakes of American and European monetary systems. When the water level in these lakes rises, our puddle gets a boost and expands, and when it falls, the puddle dries up. The puddle differs from lakes in that it does not have its own sources, so the water level in it depends on the supply of water through communicating vessels from other reservoirs. Therefore, it cannot form its own ecocenosis, and the biocenosis consists of primitive organisms. Large fish and complex organisms cannot withstand periodical desiccations. The puddle could be deepened, and own water sources could be found, but the guarding monetary authorities solicitously coat it with asphalt and do not allow to disconnect the channels when the water level in neighboring lakes drops. The creation of a sovereign monetary system is hampered by dogmas firmly embedded in the way of thinking of monetary authorities. They piously believe that the system created by them corresponds to the best world standards, and any serious alteration of it will represent (in their logic of monetary reforms) a step-back. In fact, these standards were established by the Washington's international financial institutions not in connection with progress, but for reasons of convenience for the global expansion of U.S. capital, continuously fueled by the Fed through issuance of the global reserve currency. Indeed, what is so progressive in the abolition of control over cross-border movements of capital, or in a reduction of the customs tariff? After all, these are nothing more than technical tools that any sovereign state may apply to develop its economy! Moreover, the extensive experience of their application testifies to the advisability of using currency regulation tools to protect the national financial market against speculative attacks, and customs and tariff protection to serve the developing industry sectors. The same applies to the regulation of the domestic market, as the dogma of market fundamentalism proceeds from the premise that the more free is the pricing and the less is the share of state property, the more progressive is the regulatory system. Although, according to the theory and practice of market economy management, both should be determined by considerations of economic efficiency. There is no point in privatizing a state-owned enterprise, if there is no certainty that private owners will not ruin it, as did happen to most of our machine-building enterprises. It also makes no sense to abolish state control over energy tariffs in the absence of competition mechanisms or consumer participation in their establishment. This, in particular, is clearly stated in American manuals on the theory of management, which prioritize the criterion of economic efficiency. The list of such examples of deliberate ideologization of macroeconomic regulation tools could go on and on. For example, the author's proposal to peg the ruble exchange rate for ending the artificially created panic in the foreign exchange market caused a real stir among the advocates of the pursued policy. They united in defense of the mechanism that created the speculative foreign exchange funnel, as if they had shared among themselves the multibillion-dollar profits obtained by speculators in the game against the ruble. Meanwhile, this proposal was made on the basis of common sense and taking into account the rich international experience of repelling speculative attacks in different developing countries. It rested on simple calculations that in the current circumstances, the costs of defending against a speculative attack using such a method would be an order of magnitude smaller than the losses of savings of the state and the population, which occurred as a result of the transition to a floating ruble exchange rate and its subsequent crash. Apart from commercial interest and involvement in the manipulation of the market, certain conspiracy theorists offer another simple explanation of the regulator's logic. They regard it as a hidden form of indemnity paid by post-Soviet states as a result of their defeat in the Cold War. This idea is usually proved by calculation of losses of our economy as a result of reforms and acquisitions of the U.S., the balance of which is estimated at more than a trillion dollars of relocated capital, hundreds of tons of priceless materials, and hundreds of thousands of migrated intellects. We can add to this internal losses represented by a multiple fall in the production of high-tech goods, demolition of entire branches of science-intensive industry, as well as reduction and degradation of the population. However, simplicity does not eliminate the need for factual evidence. In addition, in recent years there arose a counterexample of the independent foreign policy of the Russian leadership. At the same time, the effectiveness of economic sanctions proves that within the current economy regulation system, Russia is too vulnerable to American threats to be truly independent[241]. The truth is that economic policy is a function of economic interests. More precisely, the interests of economic entities possessing political influence. They do not necessarily have to coincide with the national interests. History has many examples of comprador conduct by business elites in developing countries, ensuring the implementation of a policy of servicing the interests of foreign capital, rather than the development of national productive forces. Let's not forget that the Russian oligarchy, which arose on the wave of privatization of state property, organized a coup in 1993 in order to preserve the Yeltsin regime that had given birth to it. In an effort to insure against changes of this regime, a significant part of oligarchic business was transferred to offshore, withdrawing property rights from Russian jurisdiction. Thus, the oligarchy ended up in external dependence and inevitably became comprador. A convincing example of such dependence is the recent coup d'é tat in Ukraine, during which the U.S. secret services manipulated leading Ukrainian businesspersons, including partners of the deposed president. There is no doubt that the offshore oligarchy is interested in maintaining the existing system of macroeconomic regulation. Although the introduction of anti-Russian sanctions results for many Russian capitalists in a cessation of business refinancing and even puts it on the verge of bankruptcy, for the most part they are not yet ready to exchange their offshore paradise for refinancing by the Bank of Russia, which cannot be compared with foreign sources in terms of inexpensiveness and maturity. The scope of the Russian economy offshorization is unprecedented, since about a trillion dollars of Russian business assets have been withdrawn to offshore zones, half of which continue to participate in the reproduction processes, providing 85% of the foreign investments received by Russia. Annually, the reproduction of fixed capital by means of offshores amounts to about $ 50 billion (Fig. 20).

Fig. 20. Offshorization of the Russian economy Notes: *) FDI from the Russian Federation includes capital flight (volumes in the relevant years) **) FDI flow to the RF – FDI attracted net of repaid (repatriated by non-residents); FDI flow from the RF – FDI sent abroad net of repaid (Source: Y. Petrov) A repatriation of the offshore oligarchy is necessary not only to increase the efficiency of the Russian financial system, but is objectively conditioned by threats of economic sanctions that can instantly block most of these assets located within U.S. or British jurisdiction. Therefore, the replacement of external sources of credit with domestic ones must be accompanied by the return of offshore assets to Russia. However, during the past financial crisis, some of the offshore oligarchs contrived to obtain hundreds of billions of rubles of unsecured loans from the government and " earn" super-profits from speculation against the ruble without any encumbrances and obligations, and even to transfer these super-profits to offshores. For this reason, they hastened to create the illusion of a successful anti-crisis policy in the halls of power and the media, although Russia ranked last in the G20 in terms of GDP, industrial output and investment[242]. Today they want to repeat this trick with the monetary authorities, getting public funds without assuming any obligations. Resolutions have already been adopted for 2 trillion rubles for capitalization top-up of several dozen entities, including private ones. A proximity to high-ranking officials who carry out " manual management" of anti-crisis money allows them not to worry about the general macroeconomic consequences of the current policy, which for the vast majority of business entities does not promise either loans or profits. We could stop here the explanation of the reasons for such strange survivability of the pursued macroeconomic policy. Indeed, if the leading economic power of the country is offshore oligarchy under Anglo-Saxon jurisdiction, then one cannot be surprised at the justification of a monetary policy that is harmful to the national economy. For the interests of offshore business, maintaining the full openness of the financial system is more important than creating internal sources of credit. All the more so, if in case of need one can make an arrangement with the state credit distributors on individual conditions. These interests explain obsessive unsubstantiated mantras about the obsolescence of certain forms of economic regulation, and impossibility of any other way except for the consistent and irreversible liberalization of the economy. The dogmas of market fundamentalism are foisted on under the guise of supposedly scientific but secret knowledge, accessible only to monetary authorities. Despite the fact that this " secret knowledge" is represented in junior grade textbooks of economic schools as primitive models of market equilibrium, and their consistence with reality is refuted both by objective scientific research and practical experience, it is considered a bad form for the ruling elite to doubt the dogmas of market fundamentalism. Therefore, along with a materialistic explanation of the reasons for the pursued macroeconomic policy consisting in economic interests of the offshore oligarchy, it is necessary to discover the epistemological prerequisites for its vitality. It is these features of religious thought that have manifested themselves in the behavior of monetary authorities in recent months. Initially, the adherents of market fundamentalism persuaded the leadership to convert to a policy of inflation targeting, misleading it by casuistry. After all, inflation targeting is actually understood not as a system of measures to achieve an inflationary goal, as it might appear from the word " target, " but as reduction of the entire range of monetary policy tools to key rate manipulation in the hope of achieving target goals for the consumer price index. After that, they announced the impossibility to combine several goals at once, although the theory of management suggests that the selective capacity of the managing system should not be lower than the variety of the management object. Contrary to this obvious principle, the leadership was convinced of the need to move to the floating ruble exchange rate, reducing the monetary policy tools to defining the key interest rate at which the Central Bank issues short-term loans to commercial banks (links to textbooks on economic cybernetics). Contrary to the opinion of both the scientific and business community, they began to raise the key rate to reduce inflation. Having received the exact opposite result, predicted by scientists and entrepreneurs, the Central Bank raised the rate even more, cutting off the monetary system from the real sector. Meanwhile, speculators who made hundreds of percent per annum on speculations against the ruble and easily accepted the increase in the key rate, sucked all the liquidity provided by the Central Bank and crashed the ruble exchange rate. Inflation soared even higher. Despite the obvious failure to achieve all the declared goals, another devaluation of the ruble savings and income of millions of citizens who trusted the state, and the huge damage inflicted on the real economy and caused by the policy pursued during the crisis, none of its authors doubted the correctness of the actions taken. The myth about inflation targeting and the refusal to control the exchange rate of the ruble is based on scholastic hypotheses centered around almost century-old observations. Let us start with the logic of monetary authorities that imposed " targeting" of inflation. If the refusal to control the cross-border movement of money on the capital account is postulated, then in the conditions of free market pricing for managing macroeconomic parameters, the monetary authorities still have control over the ruble exchange rate and monetary policy tools, which include the refinancing rate and other conditions for providing liquidity, mandatory reserve requirements, capital adequacy, provisioning for loans and securities, scope of open market transactions with government bonds and foreign exchange interventions, which together form the size of the monetary base. On this account, the scientific sources regard as proven the trilemma that in the absence of a gold standard it is impossible to simultaneously maintain an open capital market, a fixed exchange rate of the national currency, and to conduct an autonomous monetary policy. Apparently proceeding from this logic, the monetary authorities choose an autonomous monetary policy, preferring to manipulate the interest rate and sacrificing the control over the exchange rate[243]. This trilemma was formulated by Obstfeld, Shambaugh and Taylor on the basis of an empirical study of monetary policies pursued by national banks during the period between the First and Second World Wars (IMF Staff Papers, Vol. 51, 2004). However, much has changed since then. A global financial market emerged along with the world reserve currency, represented by the dollar issued by the U.S. Federal Reserve System mainly against obligations of the U.S. government. Considering that the amount of these obligations is growing exponentially and has gone far beyond the stability of the U.S. fiscal system, this trilemma should be supplemented by a " lemma" on the growing issuance of global capital in the form of unsecured obligations of the American state. For the sake of precision, they should also be supplemented by unsecured obligations of the EU countries (Greece, Great Britain, etc.), along with which the issuance of euro and pound is growing, as well as Japan with parallel yen issue. The issue of these quasi-reserve currencies grows exponentially following the dollar, which resulted in a 3-5-fold increase in the mass of these currencies in the world financial market over the period after the onset of the global financial crisis in 2008. Thus, unlike the interwar period, the modern capital market is characterized by the pattern of its growing inflation (swelling) at the expense of unsecured issuance of world reserve currencies. Therefore, the countries that keep the capital market open are inevitably exposed to pressure, boundless and increasing issuance of these currencies in the form of boundless flows of speculative capital. This means the appearance on the world financial market of a monopoly that has enormous opportunities for manipulating it, also by establishing control over the national segments of the world financial system that are open to free movement of capital. Unlike the world market of goods that obeys the laws of competition and is regulated by WTO rules, the global financial market is not regulated for real, and IMF standards only protect this deregulation in the interests of institutional financial speculators (investment superbanks) that enjoy unlimited access to issuers of world currencies. From what has been said above, the quadrilemma follows: if the National Bank does not have the opportunity to issue a world reserve currency and keeps an open account of the cross-border capital flow, it cannot control in its country either the exchange rate or the interest rates. Those who have access to issuance of world currencies can conduct at a suitable time a speculative attack of any capacity, crashing the exchange rate, and provide borrowers from your country with any amount of credit at an interest rate acceptable to them. In relation to Russia, they have shown this many times. The above entails that in order to manage the condition of the national currency and monetary system, it is necessary to control the cross-border movement of money for capital operations. Otherwise, the development of our economy will be determined from abroad, plunging it into an increasingly chaotic state. Managed chaos will also feed the Russian oligarchic offshorized business groups, trying to derive super-profits from economy destabilization. As a matter of fact, this is the essence of the transition to a policy of " targeting" inflation. While politically the so-called " targeting" of inflation means nothing but transfer of control over the condition of the national monetary and financial system to external forces (primarily the U.S. Federal Reserve, the Bank of England, the ECB and the Bank of Japan), economically this is done in the interests of foreign financial speculators (TNCs and foreign banks, oligarchic offshorized business groups the beneficiaries of which have long become international investors and even " global citizens" ). If the state loses control over the exchange rate of its currency, it means that it gives up its manipulation to currency speculators. And in the situation when the Central Bank extends credit to them, and the financial controller transfers the currency exchange under their control, one can witness emergence of " currency swings, " the currency and financial market enters a state of turbulence, all foreign trade activities become disrupted, with a disarray in the reproduction of enterprises dependent on it. This is exactly what happened in the Russian economy as a result of the policy of " targeting" inflation. Thus, the entire concept of inflation targeting is nothing more than a pseudo-scientific hoax, launched in the interests of international speculative capital. No great wonder that the policy of the Central Bank in 2014 resulted in making the currency speculators, who profited from the devaluation of the ruble, and now continue to cash in on its revaluation, leaders in profit-making. During the entire last year, the profitability of currency speculations against the ruble amounted to tens of percent per annum, and after letting the ruble rate float free, it spiked on certain days to a hundred percent and more. At the same time, the profitability of the manufacturing industry dropped to 5-7%, and solvency of real sector enterprises fell significantly. The terms of their lending have been consistently worsening as the Bank of Russia increased the key rate. After it was raised to 17%, credit became unavailable for most enterprises in the real sector, and the liquidity remaining in the economy rushed to the foreign exchange market. Its subsequent collapse was the natural result of both manipulation of it and the policy pursued by the monetary authorities. This year, the policy of stimulating currency speculation continued. To reduce the demand for currency on the exchange, the Bank of Russia has deployed a mechanism for refinancing in foreign currency under currency repo transactions. In so doing, it created a new channel for enriching of speculators, now on the rise of the ruble rate. Taking foreign currency loans at 2%, banks convert them into rubles, buying federal loan bonds at 10%, and then sell them and convert again into foreign currency at the already increased ruble exchange rate. Given its increase by a third, it is easy to calculate that the profitability of these speculations was the same 30-40% as in the previous year on the smooth decline of the ruble exchange rate. One of the financial structures on familiar terms with the monetary authorities " earned" almost a billion dollars in a flash using currency repo transactions for jobbery with Russian Eurobonds. Not surprisingly, money continued to flow into the currency and financial market, leaving the real sector. Only in the first quarter, the volume of loans issued by banks to industrial enterprises fell by almost half a trillion rubles. Accordingly, the financial situation of enterprises continued to worsen. According to operative data of the Russian Federal State Statistics Service, in January of 2015 the net operating loss of Russian organizations amounted to 152.5 billion rubles. The share of loss-making enterprises reached in the Russian economy on the average 36.1%. At the same time, the largest share of unprofitable production facilities is recorded in manufacturing sector (39.9%). In real terms, net profit of manufacturing facilities fell to the 2001 mark. It is worth noting that the largest operating losses are recorded in manufacturing enterprises (about 506.4 billion rubles), which have not been able to take advantage of the increased competitiveness of their products due to the devaluation of the ruble because of extremely stiff and suffocating monetary policy. Despite all the appeals of the country's leadership to achieve extensive import substitution and use the increased price competitiveness of domestic products after the devaluation of the ruble to expand production, in actual life it did not come off due to lack of credit. Worse yet, the portfolio of ruble loans issued to the real sector decreased by 410 billion rubles over the first quarter of 2015, and the share of overdue debt on ruble loans to the real sector as of May 1 of this year increased by more than 60% compared with the beginning of 2014 (in particular, by 27% since the beginning of 2015), reaching almost 7% of this segment of the loan portfolio. This is not surprising, given that the real sector, especially machine building, has had access to ruble credit resources at least in the first quarter of 2015 at about 20% per annum, which is almost double the Bank of Russia's expectations for annual inflation.

|

Последнее изменение этой страницы: 2019-06-09; Просмотров: 163; Нарушение авторского права страницы