|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

|

|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

Defeat of the Russian economy by external manipulation of its regulators

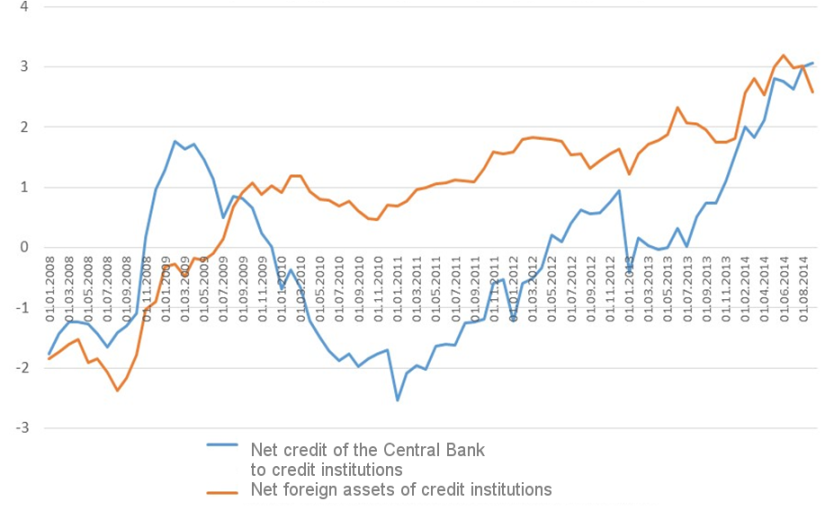

The sanctions were aimed at the financial system, the part of the existing reproduction system that was most vulnerable and dependent on the outside world. The refusal of Western banks to refinance previously issued loans significantly aggravated the export of capital and created macroeconomic conditions for a speculative attack against the ruble. Before that, it had been prepared by the actions of the monetary authorities to transfer the ruble to the " free float" regime, which had created expectations of its devaluation. Hastily disclaiming responsibility for maintaining a stable ruble exchange rate, they provoked under the imposed sanctions a speculative attack against the ruble, which was immediately arranged by the currency exchange. The role of the Moscow Exchange (MOEX) in the crash of the ruble rate deserves special analysis. Its management failed to take even a single action from the standard set of measures that they were required to take in order to stop the frantic run from the ruble, starting with suspension of trading and reduction in the number of sessions, and ending with termination of credit leverage application and virtual transactions. However, as evidenced by sophisticated speculators, at the beginning of the rise of the wave of feverish getting rid of rubles, the exchange, on the contrary, suspended the acceptance of applications for their purchase due to a " technical malfunction, " thereby sharply intensifying this wave. On this wave, the speculators supervising exchange transactions had no problem in dropping the ruble by more than 10% through several feigned deals, boosting the profitability of their operations to 1, 000% per annum. This is all the more evidenced by the spicy circumstance that the bulk of these transactions accrued to two structures only. While MOEX was a " daughter of the Central Bank" and acted as a key element of the market infrastructure under its control, stabilization mechanisms were applied regularly. But after privatization, it started operating as a profit center run by professional speculators associated with the largest U.S.-European and Russian financial conglomerates. Conspicuously, the two companies that had performed most of the transactions which crashed the ruble exchange rate enjoy a special confidence of the regulator, which recently granted to one of them an unprecedented financial assistance for rehabilitation of a dingy bank. Another of them was admitted to the market, despite the fact that its chief executive had been deprived of the license to carry out operations. As is well known, speculators derive super-profits from destabilizing the market, so the monetary regulators of all countries are constantly combating them, strictly suppressing attempts to bring the market out of balance. The Russian regulator, on the contrary, has yielded the market to the mercy of speculators. Controlling the exchange, they occupy a monopoly position in the monetary and foreign exchange market, arbitrarily forming prices through chains of feigned transactions. Faced with increasing speculative pressure on the foreign exchange market, the Bank of Russia, instead of stopping the speculative wave via banking and currency control tools, has only multiplexed it by providing short-term refinancing to commercial banks (Fig. 18). Fig. 18. Dynamics of private foreign assets and net debt of credit institutions to the CB RF (trillion rubles)

They lent this money to affiliated players, which allowed the latter to increase the scope of speculative transactions by using an 8-fold credit leverage[235]. Objectively, the Russian financial system could have easily defended itself against sanctions, having a significant and stable positive trade balance and large foreign exchange reserves that exceeded the monetary base almost twofold[236]. However, remaining in the system of rigid restrictions established by the IMF to open up the Russian financial system for the free movement of capital, the monetary authorities not only failed to repel the speculative attack against the ruble, but also strengthened it. In fact, the monetary authorities played into the hands of foreign speculators who attacked the ruble after the decision of U.S. President Obama to impose economic sanctions. Direct confirmation of the strict observance by the Russian monetary authorities of the prescriptions issued by overseas " gurus" is found in the conclusion of the IMF mission in Russia, published on October 1, 2014[237]. After reading this document, which contains direct instructions to the Bank of Russia (in bold), the reasons for the strange behavior of the Central Bank become understandable. " Geopolitical tensions are slowing the economy already weakened by structural bottlenecks. In this environment, maintaining sound macroeconomic policies and frameworks would help limit downside risks. The Central Bank of Russia (CBR) should tighten policy rates further to reduce inflation and continue its path towards inflation targeting underpinned by a fully-flexible exchange rate. While the projected overall fiscal stance is appropriately neutral in 2015, the needed fiscal consolidation should resume in the following years. The operational independence of the CBR should be safeguarded and adherence to the fiscal rule should continue. Enhancing Russia’s growth potential requires bold structural reforms and further global integration." The economic outlook appears bleak. GDP is expected to grow by only 0.2 percent in 2014 and 0.5 percent in 2015. Consumption is expected to weaken as real wages and consumer credit growth moderate. Geopolitical tensions – including sanctions, counter-sanctions, and fear of their further escalation – are amplifying uncertainty, depressing confidence and investment. Capital outflows are expected to reach USD 100 billion in 2014 and moderate somewhat but remain high in 2015. Inflation is projected to remain over 8 percent by the end of 2014 mostly due to an increase in food prices, caused by import restrictions, and depreciation of the ruble. In the absence of further policy actions, inflation is expected to stay above target in 2015. Despite the slowdown, the economy is expected to have limited excess capacity owing to structural impediments to growth. Risks are tilted to the downside. Current projections assume a gradual resolution of geopolitical tensions over the next year. Deterioration of confidence, or an escalation or prolongation of geopolitical tensions, could lead to larger capital outflows, greater exchange rate pressure, higher inflation, and lower growth. A reduction in world oil prices could amplify this impact. Maintaining a stable and predictable macroeconomic framework is essential to underpin confidence, especially in the current environment. This includes following the fiscal rule, pursuing the inflation targeting agenda underpinned by a fully-flexible exchange rate regime, and investing the resources of the National Wealth Fund only with appropriate safeguards. Russia has substantial buffers: a large level of reserves, a positive net international investment position, low public debt, and a small general government deficit. However, given the uncertainties about the duration of geopolitical tensions and underlying structural weaknesses, using these buffers wisely is key to providing resilience to the economy. A tighter monetary stance is required to reduce inflation. The CBR has appropriately raised its policy rates in recent months while resuming the path to greater exchange rate flexibility. However, core inflation has accelerated, implying that monetary tightening is necessary to anchor inflation expectations. Higher interest rates would also help limit capital outflows – especially in an environment of tightening global liquidity – and reduce the bank funding gap by bringing real policy rates firmly into the positive territory. The CBR’s operational independence should be safeguarded. While broad ownership is desirable in setting medium-term inflation goals, the implementation of policies to reach the target should be the exclusive domain of the CBR. A clear mandate will be critical to ensure a credible transition to inflation targeting. Increased oversight and heightened financial stability remain a priority. Banks and the corporate sector are facing a challenging environment due to the weak economy, limited access to external financing, and higher financing costs. Existing financial buffers together with appropriate policy responses by the CBR have limited financial instability thus far. Nonetheless, the current uncertain environment could create difficulties in individual banks and businesses, even in the near term. In case of acute liquidity pressures, emergency facilities should be temporarily offered to eligible counterparties, against appropriate collateral, priced to be solely attractive during stress periods. In the event of market dysfunctions and excessive currency volatility, foreign exchange interventions should also be used without targeting a certain level of the exchange rate. The fiscal stance envisioned for 2015 is appropriately neutral. The proposed federal budget, which is consistent with the fiscal rule, envisions a loosening in 2015. However, this is offset by a tightening at the sub-federal levels. This strikes an appropriate balance between the need to consolidate in the medium term, with the non-oil deficit remaining near historical high, and the need for supportive fiscal policy in the face of the current downturn. Adherence to the fiscal framework is essential. The fiscal rule should become a cornerstone of the credibility of macroeconomic institutions. Russia should resist mounting spending pressures and preserve fiscal space for public investment to meet its large infrastructure needs. The use of the National Wealth Fund for domestic infrastructure projects may be appropriate to consider if done in the context of the budget process and subject to appropriate safeguards. The diversion of contributions from the fully-funded pillar weakens the viability of the pension system, creates disincentives to save, and dilutes the credibility of the fiscal rule. Structural reforms are essential in the face of growing uncertainty. Sanctions, counter-sanctions, and heightened uncertainty are leading to additional state interventions in the economy, slowdown in the structural reform agenda, and decreased global integration. Measures to mitigate the impact of geopolitical uncertainties should avoid amplifying existing distortions in the economy. Even if uncertainty dissipates next year, domestic demand and potential growth are projected to remain weak in the medium term due to insufficient investment and deterioration in productivity. Potential growth is projected to be about 1.2 percent in 2015, reaching 1.8 percent in 2019, with downside risks. Structural reforms are needed to provide appropriate incentives to expand investment and allocate resources to enhance efficiency. Protecting investors, reducing trade barriers, fighting corruption, reinvigorating the privatization agenda, improving competition and the business climate, and continuing efforts at global integration remain crucial to revive growth." So, the administration of the Bank of Russia pursues a policy that actually is not independent, but imposed by the IMF. The IMF, in its turn, serves the interests of the U.S. and is supervised by the U.S. Treasury. It is the latter that manipulates the Bank of Russia by introducing approaches to the monetary and credit policy that are appropriate to the U.S.-centric global economic order. This includes broadcasting through the IMF of requirements to renunciate currency regulation and control over cross-border capital transactions. It is open to guesswork whether the management of the Bank of Russia were aware of the destructive consequences of the decisions they made, or Americans used them in an unwitting fashion, employing the dogmatic schemes of thinking embedded in their minds. Anyway, the monetary authorities supported the attack of speculators against the ruble with multibillion loans through a mechanism of short-term refinancing, which caused the currency rate crash unprecedented in the modern world. After that, guided by the monetarist dogma, they jacked up the key interest rate and actually cut off credit from the real economy sector, suffocating economic growth. Demand for money sagged and, simultaneously with the money supply squeezing, the fall in investment and production began. Introducing economic sanctions, the U.S. reckoned upon exactly this behavior of the Russian regulator. The U.S. rating agencies supported this ultimatum by reducing the Russian credit rating almost to " junk" grade. These circumstances will obviously whip up the export of capital. Unless the policy of the monetary authorities is changed, we can confidently predict a further deterioration of the Russian economy. Considering that it will be necessary to repay to external creditors another $ 150 billion before the end of 2015, the monetary base may be further reduced by 10-15%, entailing a relevant decline in business and investment activity. The state will have to spend foreign exchange reserves or put up with the wave of bankruptcies of insolvent borrowers, which might include systemically important enterprises, among them those involved in fulfillment of the state defense order. Together with the decline in oil prices, all this creates a threat of a new ruble devaluation wave. Instead of finally activating the mechanisms for foreign exchange market stabilization, the monetary authorities came up with a new justification for their connivance with speculators, giving the later at the same time a new orientation cue, that is, exchange oil prices. It seems as if the Russian monetary authorities cling to any plausible explanation for the exchange rate drop in order to justify their passivity. Actually it is not them, but speculators who control the currency and financial market, while the Central Bank only registers convenient orientation cues for them. After cancellation of the exchange rate corridor, oil prices became such a cue, and their fall automatically pulls down the ruble. However, the main reason for the unacceptably high volatility of the ruble exchange rate was actually not the fall in oil prices, but manipulation of the market. Knowing the methodology of the Central Bank and using it as the " dummy player" in bridge, the speculators controlling MOEX play the ruble exchange rate without any particular risk, dropping it ever lower to delight of Obama and to their own benefit. None of the oil-producing countries in the world, including Nigeria, with the incomparably less developed economy, has experienced such a sharp drop in the national currency exchange rate because of the fall in oil prices (Table 9). The Russian financial and economic system has a much higher strength margin than any of the countries indicated in the table. It also exceeds them by the level of development, the degree of diversification and the capacity of the domestic market. Nevertheless, the reduction of monetary policy to servicing foreign exchange and financial speculation negates these advantages. As soon as the Central Bank raised the key interest rate to 8% exceeding the profitability of the production sphere, it switched cash flows to servicing foreign exchange and financial speculation. After it raised the rate to 17% and simultaneously started withdrawing money from the economy, offering commercial banks to place funds on deposit at 16.79% per annum, the real sector became completely disconnected from credit. The exchange became the main money attraction center in the Russian economy, concentrating all liquidity within itself and thus forming a giant speculative funnel. Over the past year, the volume of transactions performed on it was 10-fold greater than the total exports of the country, and 5.5-fold greater than the total debt of the state, banks and companies to foreigners. During this year, against the backdrop of falling investment and production, the turnover of MOEX doubled, and the exchange itself became the most high-grossing entity in the country, showing a profit margin of about 80%.

Table 9. Currency exchange rate dynamics in the oil-producing countries in 2014.

The entire financial and economic system of the country started revolving around MOEX, focusing on the profitability of foreign exchange transactions and serving speculators. Consequently, it became critically dependent on the behavior of the latter. This circumstance predetermined the effectiveness of U.S. sanctions, with the announcement of which international speculators rushed to bring down the ruble. With an eye to sameness of the capital movement conditions, U.S. rating agencies forecast a decline in Russian GDP this year by 4-5.5%, the World Bank gives the figure of 2.9%, and the IMF, 3%[238]. There's no doubt that such course of events can easily be avoided, as it was not difficult to prevent the currency crisis of the last year, with the economy plunging into a recession. After all, the decline in investment and production takes place against the backdrop of underutilized production capacities (Fig. 19), 20% concealed unemployment, unimplemented scientific and technical potential. The calculations of the leading experts in forecasting show the possibility of a steady growth of the Russian economy by 6-8% per year[239]. But to achieve this, monetary policy should be changed with introduction of currency regulation and control, direct and indirect methods of reducing capital outflow, extension of long-term and cheap loans to production enterprises, obliging banks to supervise their intended use. This will require abandoning the market fundamentalism dogmas and moving to a pragmatic policy of economic development based on the revitalization of the existing scientific and production potential. Relevant proposals have been repeatedly discussed in the scientific community and presented in the reports of the RAS Section of Economics[240].

(Source: the RAS Institute for National Economic Forecasts) However, before discussing them again, it is necessary to understand the reasons for such persistent continuation of the current policy, despite its obvious perniciousness.

|

Последнее изменение этой страницы: 2019-06-09; Просмотров: 168; Нарушение авторского права страницы

Fig. 19. Capacity utilization rate in 2014, %.

Fig. 19. Capacity utilization rate in 2014, %.