|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

|

|

Архитектура Аудит Военная наука Иностранные языки Медицина Металлургия Метрология Образование Политология Производство Психология Стандартизация Технологии |

Read the text and find answers to the following questions.

1) What main types of organizational structures are mentioned in the text? 2) What are the traditional ones? 3) What features does the line structure have? 4) What are the relationships in the functional structure? 5) How can the divisional structure be divided? 6) What structure is the most complex one?

Line Structure – this is a kind of structure that has a very specific line of command. The approvals and orders in this kind of structure come from top to bottom in a line. This kind of structure is suitable for smaller organizations like small accounting firms and law offices. This is the sort of structure that allows for easy decision making, and also very informal in nature. They have fewer departments, which makes the entire organization a very decentralized one.

to the functions performed by them in the organization. The organization chart for a functional based organization consists of President, Sales department, Customer Service Department, Human Resources, Accounts department and Administrative department.

The modern and comparatively new types of organizational structures are:

Product structure is based on organizing employees and work on the basis of the different types of products. If the company produces three different types of products, they will have three different divisions for these products. Market structure is used to group employees on the basis of specific market the company sells in. A company could have 3 different markets they use and according to this structure, each would be a separate division in the structure. Geographic structure – large organizations have offices at different place, for example there could be a north zone, south zone, west and east zone.

Text 2 Marrying in haste

Mergers and acquisitions continue apace in spite of an alarming failure rate and evidence that they often fail to benefit shareholders. The collapse of the planned Deutsche-Dresdner bank merger tarnished the reputation of both parties. Deutsche Bank’s management was exposed as divided and confused. But even if the takeover had gone ahead, it would probably still have claimed its victims. Most completed takeovers damage one party – the company making the acquisition. A long list of studies has all reached the same conclusion: the majority of takeovers damage the interests of the shareholders of the acquiring company. They do, however, often reward the shareholders of the acquired company, who receive more for their shares than they were worth before the takeover was announced. Mark Sirower, visiting professor at New York University, says surveys have repeatedly shown that about per cent of mergers fail to benefit acquiring companies, whose shares subsequently underperform their sector. Why do so many mergers and acquisitions fail to benefit shareholders? Colin Price, a partner at McKinsey, the management consultants, who specializes in mergers and acquisitions, says the majority of failed mergers suffer from poor implementation. And in about half of those, senior management failed to take account of different cultures of the companies involved. Melding corporate cultures takes time, which senior management does not have after a merger, Mr. Price says. ‘Most mergers are based on the idea of «let’s increase revenues», but you have to have a functioning management team to manage that process. The nature of the problem is not so much that there’s open warfare between the two sides. It’s that the cultures don’t meld quickly enough to take advantage of the opportunities. In the meantime, the marketplace has moved on. Many consultants refer to how little time companies spend before a merger thinking about whether their organisations are compatible. The benefits of mergers are usually couched in financial or commercial terms: cost-savings can be made or the two sides have complementary businesses that will allow them to increase revenues. Mergers are about compatibility, which means agreeing whose values will prevail and who will be the dominant partner. So it is no accident that managers as well as journalists reach for marriage metaphors in describing them. Merging companies are said to ‘tie the knot’. When mergers are called off, the two companies fail to ‘make it up 135 the aisle’ or their relationship remains ‘unconsummated’. Yet the metaphor fails to convey the scale of risk companies run when they launch acquisitions or mergers. Even in countries with high divorce rates, marriages have a better success rate than mergers. Mark Sirower asks why managers should pay a premium to make an acquisition when their shareholders could, invest in the target company themselves. Mr. Sirower denies he is saying companies should never make acquisitions. If 65 per cent of mergers fail to benefit shareholders, 35 per cent are successful. How can acquirers try to ensure they are among the successful minority? Ken Favaro, managing partner of Marakon, a consultancy which has worked for Coca-Cola, Lloyds TSB and Boeing, suggests two conditions for success. The first is to define what success means. ‘The combined entities have to deliver better 130 returns to the shareholders than they would separately. It’s amazing how often that’s not the pre-agreed measure of success, ‘Mr Favaro says. Second, merging companies need to decide in advance which partner’s way of doing things will prevail. ‘Mergers of equals can be so dangerous because it is not clear who is in charge, ’ Mr Favaro says. Mr Sirower adds that managers need to ask what advantages they will bring to the acquired company that competitors will find difficult to replicate. Managers need to remember that competitors are not going to hang around waiting for them to improve the performance of their new acquisition. Announcing a takeover will have alerted competitors to the acquiring company’s strategy. Given how heavily the odds are stacked against successful mergers, managers should consider whether their time and the shareholders’ money would not be better employed elsewhere.

Популярное:

|

Последнее изменение этой страницы: 2017-03-11; Просмотров: 900; Нарушение авторского права страницы

The traditional types of organizational structures characterized by having precise authority lines for all levels in the management are:

The traditional types of organizational structures characterized by having precise authority lines for all levels in the management are:  Functional structure classifies people according to the function they perform in their professional life or according

Functional structure classifies people according to the function they perform in their professional life or according

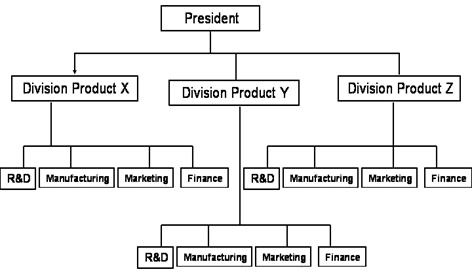

Matrix structure is a structure, which is a combination of function, and product structures. It combines both the best of both worlds to make an efficient organizational structure. This structure is the most complex organizational structure.

Matrix structure is a structure, which is a combination of function, and product structures. It combines both the best of both worlds to make an efficient organizational structure. This structure is the most complex organizational structure.